Healthcare cost pressures have officially reached a fever pitch. With annual healthcare spending projected to scale dramatically if left unchecked, Total Rewards and benefits leaders find themselves in an increasingly challenging position.

To understand exactly how rising healthcare demands are impacting organizational strategy, Grokker Innovation Labs recently issued the first installment of its 2026-2027 Healthcare Benefits Strategy Survey: Financial Strategy & ROI. The insights reveal that the era of soft metrics and VOI has been replaced by a strict corporate mandate to prove hard, actuarial ROI. However, rather than executing indiscriminate cuts, executive leadership is challenging HR teams to optimize existing networks, eliminate administrative waste, and embrace emerging AI health technologies.

Here are the five critical takeaways:

1. Pressure is rising, but strategy focuses on optimization

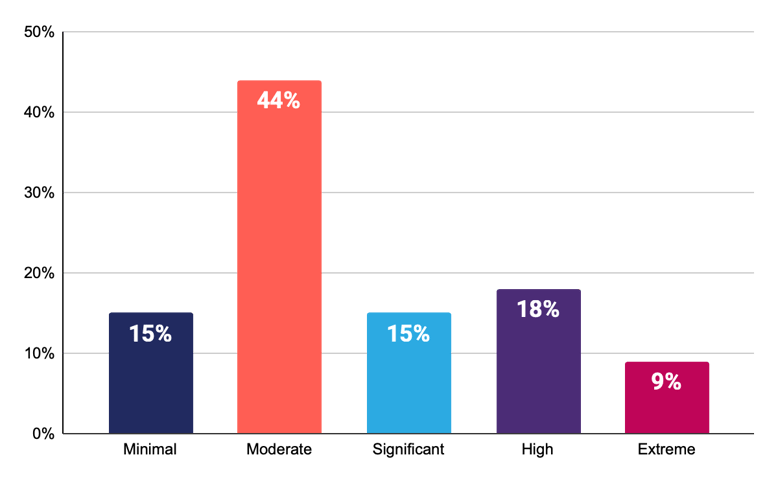

Q1: On a scale of 1 to 5, how much pressure is your executive leadership (CFO/CEO) applying to reduce total benefit spend for the next cycle?

Minimal: Business as usual; standard inflationary increases are expected and budgeted. 15%

Moderate: General guidance to "tighten the belt" and optimize vendor performance. 44%

Significant: Requirement to flat-line spend or offset increases through plan design changes. 15%

High: Strong pressure to consolidate point solutions and eliminate "PEPM bloat." 18%

Extreme: Explicit mandate to find "disruptive" savings (e.g., unbundling, RBP, or AI-Native automation). 9%

Unsurprisingly, only 15 percent of organizations are operating under a "business as usual" framework. The survey indicates that a full 85 percent of benefits leaders are actively experiencing pressure from corporate executive leadership. Specifically, 44% report moderate pressure to "tighten the belt" and optimize vendor performance, while over 40% face significant, high, or extreme mandates.

Crucially, the prevailing corporate posture is "optimize and prove" rather than "slash-and-burn." Leaders continue to view health programs primarily as strategic talent acquisition and retention tools rather than mere cost centers, meaning they prefer to exhaust careful optimization levers before considering catastrophic plan rollbacks.

2. The hard shift from VOI to actuarial ROI

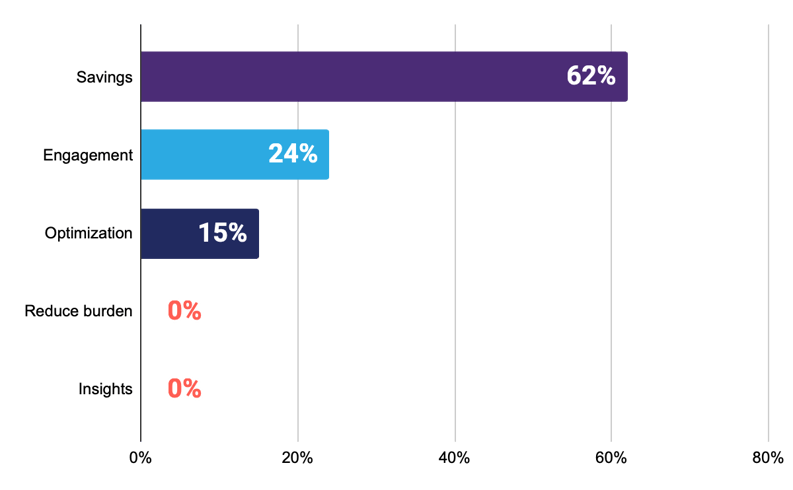

Q2: What is your top priority for improving benefits ROI in the next 12 months?

Proving measurable cost savings (claims reduction, actuarial impact) - 62%

Increasing employee engagement and utilization - 24%

Consolidating or optimizing vendors/point solutions - 15%

Reducing administrative burden on HR - 0%

Gaining real-time insights into employee needs - 0%

For years, high employee participation and registration rates were sufficient to justify vendor budgets. When asked about their top priority for improving benefits ROI over the next 12 months, a resounding 62 percent of respondents pointed directly to proving measurable cost savings, such as claims reduction and actuarial impact.

In contrast, only 24 percent prioritized traditional engagement metrics alone. More telling is that 0% of respondents selected reducing administrative burden or gaining real-time insights as primary goals. Under intense pressure to justify budgets, HR teams are willing to absorb administrative friction if it ensures immediate fiscal survival.

3. CFO conversations demand defensible data

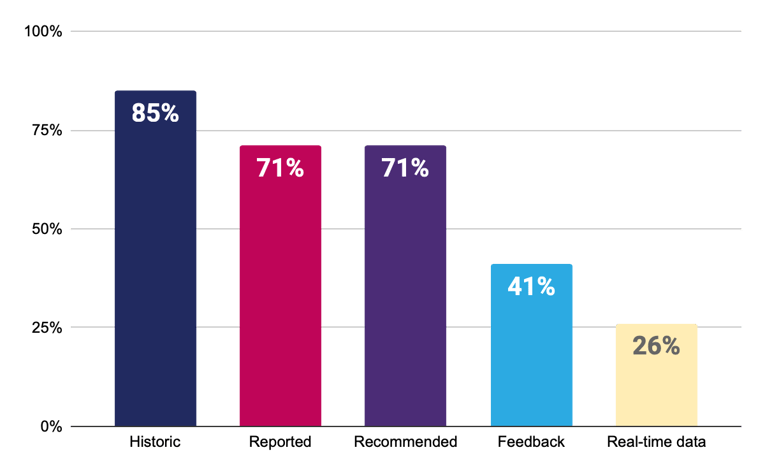

Q3: What type of data do you rely on to make benefits decisions today? (Select all that apply.)

Historical claims data (12–18 months old) - 85%

Vendor-reported engagement/utilization data - 71%

Broker/consultant recommendations - 71%

Employee surveys and feedback - 41%

Real-time or predictive data (e.g., intent, AI-driven insights) - 26%

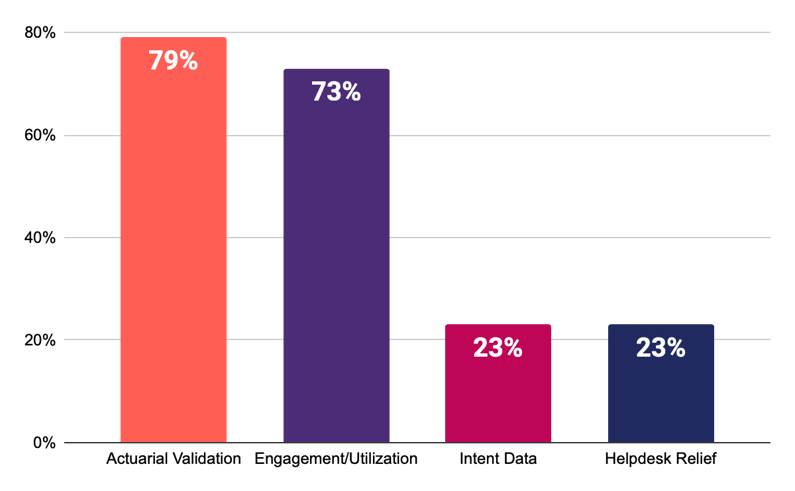

Q5: When defending your benefits budget to the CFO, how would you rank the importance of the following ROI data points? (1 = Most important, 4 = Least important)

Actuarial Validation: Proving that users of a specific solution have lower total medical/pharmacy claims costs than non-users. #1 Priority: 79% Top 2 Box Score, Weighted Score 3.26

Engagement/Utilization: Total registrations and app logins. #2 Priority: 73% Top 2 Box Score, Weighted Score 3.09

Intent Data: Seeing what employees are searching for before it turns into a high-cost claim. #3 Priority: 23% Top 2 Box Score, Weighted Score 1.94

Helpdesk Relief: Reduction in manual HR tickets and inquiry volume. #4 Priority: 23% Top 2 Box Score, Weighted Score 1.71

While softer metrics still help HR teams assess workforce expectations, they are insufficient for budget defense. The survey highlights a dual data reality: 85 percent of leaders rely on historical claims data to design strategies, and 71 percent look to vendor engagement reports.

However, when defending budgets to the CFO, actuarial validation is the absolute number one priority, securing a dominant 79 percent Top 2 Box score. Financial leaders do not trust vendor-reported "gross savings," requiring HR to tie engagement metrics back to a clear net reduction in total medical claims.

4. Traditional navigation is fragmented and vulnerable

Q7: Beyond the direct medical trend, what is the single biggest operational or financial friction point that you feel is currently unaddressed by your existing benefits partners?

Q8: If you could automate one high-touch interaction between your employees and their benefits, which one would provide the most immediate relief to your team’s workload?

In these open field response questions, benefits leaders expressed deep frustration with the current partner ecosystem, citing vendor management fatigue and severe gaps that cause manual billing errors and administrative rework. When asked which high-touch interaction they would automate to relieve their teams, leaders overwhelmingly desired automated, intelligent filters and AI-powered integrated search engines to handle basic plan inquiries.

The data indicates a clear structural shift away from portal-based static guides on an intranet toward real-time, "agent everywhere" intelligent guidance that intercepts employees directly at the point of care.

5. Vendor fatigue is a major undercurrent

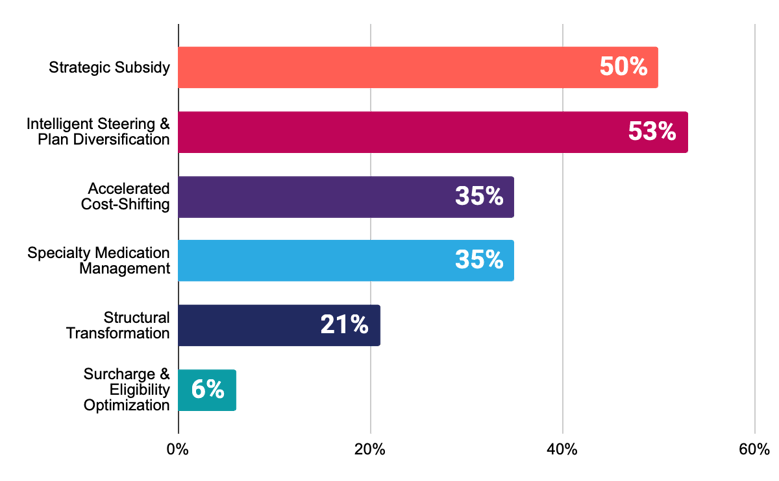

Q4: In response to the rising healthcare cost trend, please rank the following strategic levers in order of their importance to your organization's financial strategy

(1 = Top Priority, 6 = Lowest Priority).

Strategic Subsidy: We are continuing to absorb a significant portion of the cost increase to prioritize talent

retention and affordability. #1 Priority: 50% Top 2 Box Score, Weighted Score 4.50

Intelligent Steering & Plan Diversification: We are introducing alternative plan designs (e.g., Variable Copay, RBP, or Narrow Networks) to incentivize high-value provider choices without across-the-board hikes. #2 Priority: 53% Top 2 Box Score (ranked 1 or 2), Weighted Score 4.24

Accelerated Cost-Shifting: We are increasing employee cost-sharing (deductibles, premiums, or OOP maximums) to maintain our current budget margins. #3 Priority: 35% Top 2 Box Score (ranked 1 or 2), Weighted Score 3.59

Specialty Medication Management: Taking action (e.g. clinical gatekeeping, indication-based access) to better manage specialty medications (e.g., oncology, gene therapies, and GLP-1s). #4 Priority: 35% Top 2 Box Score (ranked 1 or 2), Weighted Score 3.47

Structural Transformation:We are actively moving away from traditional carrier/PBM models toward transparent, unbundled, or AI-managed ecosystems. #5 Priority: 21% Top 2 Box Score (ranked 1 or 2), Weighted Score 2.91

Surcharge & Eligibility Optimization: We are leaning into non-medical levers, such as increasing spousal surcharges, tobacco affidavits, or stricter dependent eligibility audits. #6 Priority: 6% Top 2 Box Score (ranked 1 or 2), Weighted Score 2.29

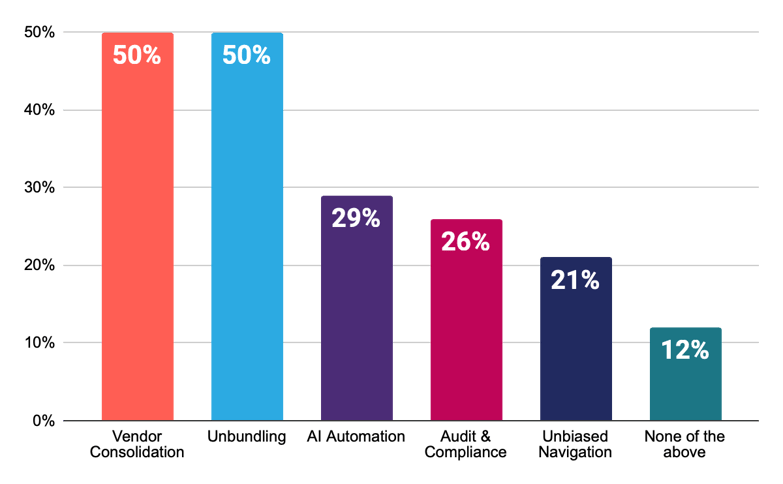

Q6: Which levers are you prioritizing to reduce 'Administrative Waste' in 2026/2027? (Select all that apply.)

Vendor Consolidation: Cutting underutilized point solutions to reduce total PEPM spend. - 50%

Unbundling: Moving away from "Big Carrier" bundles to find cheaper, niche providers for Pharmacy (PBM) or Navigation. - 50%

AI Automation: Implementing AI to deflect HR tickets and reduce manual administration. - 29%

Audit & Compliance: Running stricter dependent eligibility audits to remove non-qualifying members from the plan. - 26%

Unbiased Navigation: Moving away from vendor-biased 'front doors' toward an independent orchestrator that recommends the lowest-acuity, most cost-effective intervention regardless of the vendor. - 21%

None of the above. - 12%

Employers are "drowning" in point solutions, sparking clear vendor fatigue. This has created a strategic paradox: 50 percent of benefits leaders plan to prioritize vendor consolidation to cut PEPM bloat, while an identical 50 percent want to unbundle from big carriers to find transparent, niche pharmacy (PBM) or navigation providers.

To navigate this, 53 percent are prioritizing intelligent steering and plan diversification (such as variable copays or narrow networks) to incentivize high-value provider choices natively without cluttering the ecosystem further.

Nearly 30 percent of leaders are looking to AI automation to reduce manual administration. Instead of “biased navigation,” 21 percent say they need an independent, automated orchestrator that can sit on top of their existing stack, deflect basic support tickets, and intelligently guide employees to the right benefit at the right time.

Commanding the chaos

Ultimately, the solution for combating rising healthcare benefits costs isn't just cutting programs. It’s more an issue of gaining visibility and operational command over the entire benefits ecosystem: leveraging the right technology to help make sense of the data, supporting HR teams with actionable insights, and providing personalized benefits and care pathway guidance. Ultimately, it’s about optimizing the benefits employers are already paying for.

Want to dive deeper into the complete data set and strategic levers? Download the full Grokker Innovation Labs report here.